DPC celebrates 42 years of history in 2026

02/04/2026Paternity leave: new law provides for a gradual increase to up to 20 days

08/04/2026HIGHLIGHTS

Donations on the 2026 Income Tax Return: key points for taxpayers

The Federal Revenue Service has stepped up data cross-checks with state finance departments, resulting in a greater ability to identify discrepancies in taxpayer information

The cross-checking of donation information between the Brazilian Federal Revenue Service (RFB) and the State Finance Departments (Sefaz) occurs automatically and systematically. Tax authorities use integrated systems to verify whether the ITCMD (Tax on Transfer Causa Mortis and Donations), a state-administered tax, has been paid on donations reported on the IRPF (Individual Income Tax Return), a federally administered tax. Inconsistencies in this data may result in assessments, with the consequent collection of taxes, fines, and interest related to prior periods.

To formalize the donation of assets and rights as an advance on the statutory share, it is necessary to complete the ITCMD Statement and pay the tax corresponding to the donated amount, in accordance with the specific rules of each state.

Given this, it is essential that taxpayers carefully evaluate these transactions when preparing their 2026 IRPF return, ensuring compliance with tax requirements and reducing risks.

Donations on the 2026 Income Tax Return

An important point is that there is no income tax liability on the receipt of advance donations from an heir (inheritance). Such transactions are already taxed at the state level through the payment of the aforementioned ITCMD.

However, even though such income is classified as exempt for personal income tax purposes, these transactions must still be reported. Anyone who received a donation in 2025 must include this information in their 2026 annual tax return. The donor must also report the transaction

Furthermore, the requirement to report on the Income Tax Return is not subject to a specific minimum amount. Any transaction of this type is subject to review from a tax perspective.

This includes asset transfers such as:

- Cash donations;

- Transfers of property, such as real state, vehicles and other assets;

- Amounts received from an inheritance after the inventory is finalized.

Key points when reporting donations and inheritances on your income tax return

The Federal Revenue Service’s ability to cross-check data is growing, and this trend holds true for donations as well. The agency has stepped up its exchange of information with state finance departments (Sefaz), making it more likely to detect data discrepancies.

It is important to note that if a donation is reported to the Federal Revenue Service without the state tax having been paid, the state (Sefaz) will issue a tax assessment notice to the taxpayer.

Therefore, donations in Income Tax require attention from both the donor and the donee (the recipient). Both must ensure the consistency of the information reported.

Among the aspects that deserve attention:

- Proper identification of the parties involved (CPF or CNPJ)

- Consistency between the amounts reported by the donor and the recipient;

- Proper recording of the type of asset or amount transferred;

- Traceability of the origin of the funds, especially when they are later invested.

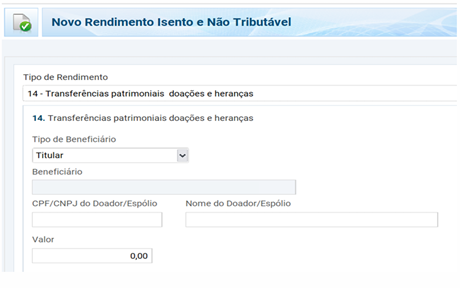

Worksheet for reporting asset transfers in the tax return

Also see: Estate Report: How does it work, when and how to submit it?

Documentation and organization of information

Another relevant aspect is document organization. To ensure greater accuracy and reliability in the Income Tax return, attention to records such as the following is recommended:

- Complete details of the parties involved;

- Documents supporting the transfer (contracts, deeds, receipts);

- Information on any applicable state taxes;

- History of the allocation of the amounts received.

DPC Private Support

The DPC Private division at Domingues e Pinho Contadores assists individuals with their tax matters, including ITCMD calculation and the preparation and filing of the Income Tax return in full compliance. Count on this support: dpc@dpc.com.br.

How can DPC help your company?

Domingues e Pinho Contadores has specialized team ready to assist your company.

Contact us by the e-mail dpc@dpc.com.br

See more

Sign up for our Newsletter:

Are you interested?

Please contact us, so we can understand your demand and offer the best solution for you and your company.

Rio de Janeiro

Av. Rio Branco 311, 4º e 10º andar - Centro

CEP 20040-903 | Tel: +55 (21) 3231-3700

São Paulo

Rua do Paraíso 45, 4º andar - Paraíso

CEP 04103-000 | Tel: +55 (11) 3330-3330

Macaé

Rua Teixeira de Gouveia 989, sala 302 - Centro

CEP 27910-110 | Tel: +55 (22) 2773-3318