Tax Reform moves forward with regulations for the CBS and IBS

04/05/2026EXPERT OPINION

Tax Reform and Split Payment: changes to tax collection procedures

Split payment changes the way taxes are collected, requiring attention to its practical aspects and an understanding of its impact on cash flow

By Fabiana Soares

As we have discussed in our previous posts, the Tax Reform introduces significant structural changes to the day-to-day operations of businesses; it is not merely a replacement of taxes. One of these major changes is the way taxes will be collected, with the adoption of split payment. This is a model already used in VAT systems in other countries and will directly impact companies’ cash flow.

Whereas today a company receives the full amount of a sale and pays the tax a few weeks later, with split payment the logic changes: part of the amount paid by the customer will be automatically set aside and remitted to the tax authorities at the time of financial settlement. This requires a fresh look at working capital management.

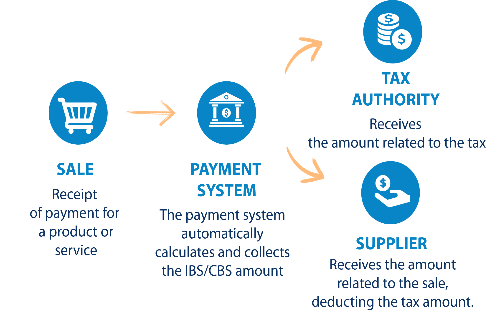

Split Payment in the Tax Reform

In practice, under this method, the IBS (Tax on Goods and Services) and CBS (Social Contribution on Goods and Services) taxes will be collected at the time the payment is made. As a result, electronic payment service providers, such as banks and payment system operators, will separate the taxes from the amount of the financial transaction between the payer and the payee and remit them directly to the tax authorities.

And this applies even to advance payments and installment plans: a portion of the tax will be collected with each installment.

Practical aspects of split payment

As mentioned, split payment provides for the automatic separation of the tax amount at the time of the transaction. However, certain aspects will vary depending on the taxpayer’s profile or the type of transaction.

It is worth noting that, in the event of the cancellation of a transaction for which the IBS and CBS have already been collected during financial settlement, the full or partial refund to the supplier of the amount collected has yet to be regulated.

Regular split payment

This is the model in which the payment provider uses the information provided by the originator of the payment transaction (tax rate, cclasstrib, etc.) to calculate and collect IBS and CBS. This model is referred to as “Superintelligent” when the payment provider is also able to check the taxpayer’s available credits to collect only the difference.

The originator of a payment transaction may be:

- the recipient (the provider of the good or service—when issuing payment slips or generating a PIX code (Instant payment system developed by the Central Bank of Brazil), for example);

- the payer (the purchaser of the good or service—when initiating a bank transfer, for example).

The originator of the payment transaction must provide the payment service provider with data that allows the transaction to be linked to the supply of goods or services, as well as the applicable IBS and CBS amounts.

In the case of a transaction facilitated by a digital platform, the platform is responsible for providing this data to the payment service provider.

Simplified split payment

If the originator of the payment transaction does not report the IBS and CBS amounts to the payment provider, this will constitute an election of the simplified split payment option. This option is no longer considered irrevocable following the enactment of Complementary Law 227/2026.

This is the model in which a fixed rate (to be determined) is used to collect IBS and CBS in the payment transaction, without the payment provider considering the actual rates applicable to the transaction or the credits available to the taxpayer.

In the assisted calculation, these collected IBS and CBS amounts will be used first to settle the taxpayer’s outstanding debts related to transactions in which the acquirer is not an IBS and CBS taxpayer under the regular regime. The remainder, if any, will be used to settle other outstanding debts the taxpayer may have.

If the payments made exceed the amounts due for the period, the IBS Management Committee and the Federal Revenue Service will refund the difference to the supplier within 3 business days after the calculation for the period is completed.

When does split payment take effect?

Although the technical documentation for the systemic implementation of payment transaction linking in certain DFe forms (Technical Note 2026.001) already exists, the implementation of split payment is scheduled to begin in 2027 (no exact date has been set yet). There is no requirement to fill out the fields related to split payment in 2026.

The published Technical Note is preparatory in nature and is intended to allow the systems of tax administrations, issuers of tax documents, and other involved parties to plan, develop, and test the necessary adaptations well in advance.

This period, therefore, is a strategic opportunity for companies to:

- review internal processes;

- adjust contracts with customers, suppliers, and financial intermediaries;

- review policies regarding payment and collection terms;

- adapt ERP and other related systems;

- train teams in tax, finance, management accounting, and IT, and promote cross-functional alignment and the definition of roles.

Cash flow impacts

This automation presents some challenges and points to consider:

- the net amount available to the company after each sale tends to be lower;

- working capital management will need to be reviewed;

- cash flow forecasts will need to account for the effect of split payment on each payment method.

On the other hand, split payment in acquisition transactions ensures faster credit (since credit is only released once the tax is paid).

How DPC can help your business

Count on DPC’s expert support to analyze the impact of split payment on your business, assist you in adapting your procedures, and guide you in developing a tax strategy aligned with the reform. Contact our team: dpc@dpc.com.br.

Author:

Fabiana Soares, partner at Domingues e Pinho Contadores and leader of the Tax Reform Working Group.

How can DPC help your company?

Domingues e Pinho Contadores has specialized team ready to assist your company.

Contact us by the e-mail dpc@dpc.com.br

See more

Sign up for our Newsletter:

Are you interested?

Please contact us, so we can understand your demand and offer the best solution for you and your company.

Rio de Janeiro

Av. Rio Branco 311, 4º e 10º andar - Centro

CEP 20040-903 | Tel: +55 (21) 3231-3700

São Paulo

Rua do Paraíso 45, 4º andar - Paraíso

CEP 04103-000 | Tel: +55 (11) 3330-3330

Macaé

Rua Teixeira de Gouveia 989, sala 302 - Centro

CEP 27910-110 | Tel: +55 (22) 2773-3318