Expatriates: companies can benefit from social security agreements

26/08/2021BEm: program that authorized salary reduction or contract suspension ended on 08/25

27/08/2021EXPERT OPINION

Functional currency: adaptation is a strategic step for the client's business

By Renata Goldoni and Rejane Xavier

An entity's functional currency is the currency of the main economic market in which the entity operates. Thus, an entity may adopt a functional currency different from its national currency to keep its corporate accounting.

The matter deserves the attention of financial administrators and managers, because if the functional currency is not the one that reliably represents the main economic environment, the company may not present appropriate reports for stakeholders' asessesment.

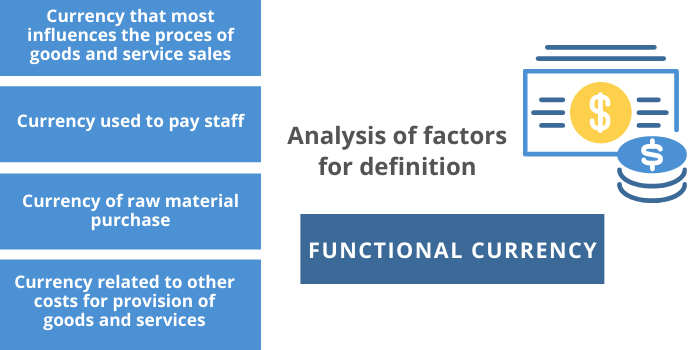

Important definitions that need to be considered in the applicability of the functional currency

Monetary items – Existence of a right to receive or an obligation with fixed value of currency. Example: loans, sales, financing.

Non-monetary item – Absence of right to receive or obligation to deliver a fixed number of currency. Example: intangible assets, inventory, PP&E.

Who does it apply to?

Any company that identifies in its operations a functional currency different from the market in which it operates must adopt a functional currency in accordance with the rules stated in Technical Pronouncement CPC 02 - Effects of Changes in Exchange Rates and Conversion of Financial Statements.

The standard establishes how a company should include foreign currency transactions and foreign operations in the financial statements and how the conversion of financial statements to a reporting currency should be done.

This is when an accounting consultancy is needed to define the best operating structure of the business for the applicability of the functional currency.

Determining the functional currency

This definition must take into account the reality of the company, the economic context in which it operates. It is not a simple choice or option. The assessment must be careful, involve the business management and be supported by specialists who have a global view of accounting processes. The entity must consider a number of factors in determining its functional currency, including:

"(a) the currency:

(i) which most influences the selling prices of goods and services (usually it is the currency in which the selling prices for its goods and services are expressed and settled); and

(ii) of the country whose competitive force and regulations most influence the determination of sales prices for its goods and services;

(b) the currency that most influences factors such as labor, raw materials and other costs for supply of goods or services (usually it is the currency in which such costs are expressed and settled)”.

Those are the primary factors. Other secondary factors and additional variables in determining the foreign entity's functional currency should also be considered.

This is just a hypothetical situation and the process is not always so obvious. An analysis of all factors is required to assess which currency most accurately represents the economic effects of transactions and events.

This definition must be well grounded in accordance with specific criteria of the rule, because the management must justify in its financial statements, in the accompanying notes, the reason for adopting a certain functional currency.

After the premises for adopting a functional currency other than the local one are defined, there should be no changes, unless there are changes in the elements and premises that defined it.

It should be highlighted that, for tax purposes , the recognition and measurement of assets, liabilities, revenues, costs, expenses, gains, losses and income must be made based on the tax accounting represented by the national currency.

Functional currency and SPED

At the operational level, it is necessary to consider that the functional currency registration is used in the preparation of the Digital Accounting Bookkeeping (Escrituração Contábil Digital - ECD). Later, these same data will compose the Tax Accounting Bookkeeping (Escrituração Contábil Fiscal - ECF).

Properly providing information in government bookkeeping is essential, as failures or omissions can lead to penalties and fines.

DPC supports companies on functional currency issues

With a strategic and integrated view of accounting processes, specialists from Domingues and Pinho Contadores support the business administration in determining the functional currency, setting up systems for correct classification, analyzing data, preparing and submitting all obligations related to functional currency.

Renata Goldoni

Rejane Xavier

Authors: Renata Goldoni and Rejane Xavier, partners at Domingues e Pinho Contadores.

How may DPC help your company?

Domingues e Pinho Contadores has a specialized team ready to assist your company.

Contact us by email at dpc@dpc.com.br

See more

Sign up for our Newsletter:

Are you interested?

Please contact us, so we can understand your demand and offer the best solution for you and your company.

Rio de Janeiro

Av. Rio Branco 311, 4º e 10º andar - Centro

CEP 20040-903 | Tel: +55 (21) 3231-3700

São Paulo

Rua do Paraíso 45, 4º andar - Paraíso

CEP 04103-000 | Tel: +55 (11) 3330-3330

Macaé

Rua Teixeira de Gouveia 989, sala 302 - Centro

CEP 27910-110 | Tel: +55 (22) 2773-3318