DPC presents the Transparency and Gender Pay Equity Report – 2st Semester 2025

25/09/2025Maternity leave period extended in case of hospitalization

13/10/2025HIGHLIGHTS

Brazilians transferred abroad: how taxation works and what are the expatriate's tax obligations

Those who leave Brazil on an overseas assignment can reduce costs and tax risks by carrying out tax planning

The transfer of a Brazilian citizen to work abroad is usually a great professional opportunity. However, expatriates on mobility need to be aware of their tax obligations in Brazil. How is income taxed in the case of international transfers?

The first point is the recommendation that professionals plan this move through tax planning, which can help reduce costs and tax risks while staying in another country.

This study considers rules and agreements between the countries involved in the expatriation process and the particularities of the individual's situation, such as sources of income, assets, and investments, in addition to their objectives.

It is good practice for multinationals to provide this type of guidance to employees who are being transferred. This is a way to provide employees with greater peace of mind and satisfaction with the process, positively impacting their experience and performance at work.

See also:

- Expatriate management: planning minimizes risks and cuts costs for companies and foreigners in Brazil

- Brazilians abroad: companies must be mindful of legal requirements

Tax Residency

The concept of tax residence is fundamental in the expatriation process. Classification as a resident or non-resident in Brazil will have a direct impact on how the individual will be taxed. This aspect must be included in the planning, in order to ensure compliance with tax rules and avoid double taxation.

Split payroll: How will expatriates be taxed?

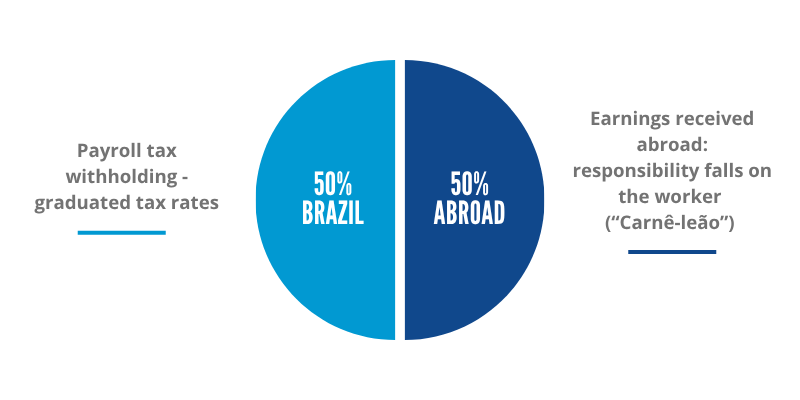

Split payroll is a method whereby part of the salary is paid in Brazil and another part abroad. This “division of the payroll” can be done at any percentage, as agreed between the employee and employer. As an example, below, we will consider that the professional receives 50% in Brazil and 50% abroad.

Income taxation is also affected by tax residency status:

Split payroll for tax residents

If the transferred Brazilian maintains tax residency in Brazil, the portion received locally is subject to payroll withholding, under the same rules applied to an employee working within Brazilian territory.

On the other hand, the income effectively paid by the employer abroad is subject to taxation in Brazil through the carnê-leão (Monthly income tax payments) system, under the responsibility of the individual taxpayer.

It is worth noting that the portion received abroad must be included in the payroll for the purposes of collecting social security contributions – INSS (National Institute of Social Security) and FGTS (Government Severance Indemnity Fund for Employees).

Split payroll for non-tax residents

When a Brazilian expatriate terminates their tax residence by filing a notice of departure, but part of their remuneration is paid in Brazil, it will be taxed at a flat rate of 25%.

But what about remuneration received abroad? This portion will be exempt from taxation in Brazil because the Brazilian expatriate has terminated their tax residence and, therefore, the income they receive abroad is not taxable here.

Regarding the portion paid in Brazil, the taxation of the non-resident will always occur through withholding at source, as established by the legislation.

Tax obligations of expatriates

Tax Resident

- Pay monthly income tax on remuneration, including amounts received abroad (carnê-leão);

- File an Annual Income Tax Return;

- Submit the Statement of Brazilian Capital Abroad to the Central Bank (when applicable)

Non-Tax Resident

- Carry out the procedure to terminate tax residency when leaving the country;

- Appoint a tax resident attorney-in-fact in Brazil to represent them before the authorities;

- Inform Brazilian paying sources about the new non-tax resident status to mitigate inquiries from the Brazilian Federal Revenue Service.

An expatriate who has a bank account in Brazilian reais but is moving abroad may maintain an account in Brazil; however, it must be under the CNR (Non-Resident Account) category, provided it is with an institution authorized to operate in the foreign exchange market.

International Agreements

Brazil maintains a series of agreements to avoid double taxation and prevent tax evasion. The texts of these treaties share similarities but may vary in detail, therefore requiring careful reading and case-by-case evaluation.

It is important to carry out this analysis during the expatriation planning phase, as it can eliminate double taxation for the professional.

There are also international social security agreements. These agreements are very important for:

- that the individual maintains their social security contributions solely in Brazil, but is also eligible for social benefits in the destination country (obviously in accordance with the terms of the applicable agreement); or

- that the contribution period in the destination country is considered for retirement purposes – totalization of periods.

Advice for expatriates and companies

One of DPC's areas of expertise is advising companies and professionals on expatriation. You can count on our support to design the entire process and tax planning, taking into account the particularities of each transfer and the unique needs of our clients. Contact us at: dpc@dpc.com.br.

How DPC may help your company?

Domingues e Pinho Contadores has specialized team ready to assist your company.

Contact us by the e-mail dpc@dpc.com.br

See more

Sign up for our Newsletter:

Are you interested?

Please contact us, so we can understand your demand and offer the best solution for you and your company.

Rio de Janeiro

Av. Rio Branco 311, 4º e 10º andar - Centro

CEP 20040-903 | Tel: +55 (21) 3231-3700

São Paulo

Rua do Paraíso 45, 4º andar - Paraíso

CEP 04103-000 | Tel: +55 (11) 3330-3330

Macaé

Rua Teixeira de Gouveia 989, sala 302 - Centro

CEP 27910-110 | Tel: +55 (22) 2773-3318