Law that makes opening companies easier and modernizes the business environment is sanctioned

31/08/2021Occupational safety and health data must be sent to eSocial as from October

09/09/2021HIGHLIGHTS

Income Tax Reform: Chamber approves text that changes taxation for individuals and legal entities

A set of measures that brings changes to the Income Tax and CSLL rules will still go through the Senate and the presidential sanction/veto

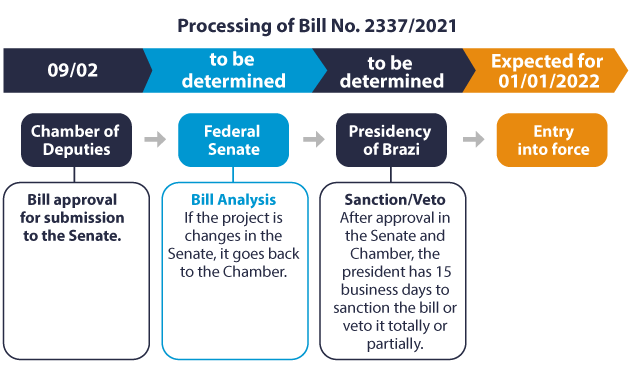

On September 2, the Chamber of Deputies completed the approval of Bill No. 2337/2021, a set of measures called the “Income Tax Reform”. The text brings changes in the rules for taxation of individuals and legal entities.

What has been proposed so far may change during the process, but following up on the topic helps to outline an idea of what is expected in the tax field.

Check the main points of the text:

Individual Income Tax

Exemption range

One of the main points is the readjustment of the income tax exemption range for individuals. The amount will go from BRL 1,903.98 to BRL 2,500.00 per month.

Update of the individual income tax table

Without changes since 2015, the table will have the following adjustment:

Current |

Income Tax Reform |

Rate |

|

Up to BRL 1,903,98 |

Up to BRL 2,500 |

0% |

|

From BRL 1,903.99 to BRL 2,826.65 |

From BRL 2,500.01 to BRL 3,200.00 |

7.5% |

|

From BRL 2,826.66 to BRL 3,751.05 |

From BRL 3,200.01 to BRL 4,250.00 |

15% |

|

From BRL 3,751.06 to BRL 4,664.68 |

From BRL 4,250.01 to BRL 5,300.00 |

22.5% |

|

Above BRL 4,664.69 |

Above BRL 5,300.01 |

27.5% |

What about the possibility of simplified declaration?

All individuals may opt for the simplified declaration model. A maximum amount of BRL 10,563.60 was set for the use of a discount. The limit currently in effect is BRL 16,754.34. This reduction in the simplified discount limit aims to replace the collection losses with the readjustment of the individual income tax progressive table.

Property value update

Today, the original property values must be maintained in the declaration. In case of sale, the tax payable varies between 15% and 22.5% on the capital gain.

After the reform, updating property values is allowed, even if the sale does not take place. A 4% rate will be charged on this upgrade.

Assets and rights abroad

Assets and rights abroad, declared up to 2020, may be updated at the rate of 6% on the capital gain.

Real Estate Funds

The text maintains exemption from income tax on income from real estate investment funds (fundos de investimentos imobiliários - FIIs).

Withholding of income tax on investments: open and closed-end funds

In the current scenario, it works like this: open-end funds pay taxes, the mandatory withholding of income tax on investments (called “come-cotas”), in May and November; closed-end funds are only taxed at the time of redemption.

After the reform, both types of funds will pay an annual "come-cota", in November. For closed-end funds, the annual "come-cota" taxation will have a 15% rate, with the possibility of paying a tax on the “stock” at the rate of 6%.

FII, FIAGRO, FIP, FIA, FIDC, among other funds, will continue without charge for "come-cotas".

Stock Exchange

The text changes the limitation for exemption of income tax on share sales. The limit goes from BRL 20 thousand a month to BRL 60 thousand per quarter. Another important change is that loss offset becomes free between the types of operation in the financial market.

Change in income tax rate for legal entities

According to the bill, the Corporate Income Tax will be reduced from 15% to 8%. The new rate would already be applied in 2022.

Reduction in CSLL for companies

The text establishes a decrease of up to 1 percentage point in the CSLL (Social Contribution on Net Income) collection. The reduction will be 0.5 percentage point in two stages, linked to the reduction of tax deductions that will increase the collection. The total will reach 1 percentage point:

- 9% to 8% in general cases;

- 20% to 19% for banks;

- 15% to 14% for other financial institutions.

Review of tax benefits

As a way of compensating the loss in government revenue, the bill includes the elimination of some tax benefits:

- exemption from income tax on housing assistance for public agents;

- presumed credit for medicine producers and importers;

- reduction to zero of rates for certain chemical and pharmaceutical products;

- exemption for natural gas and coal-fired thermoelectric plants.

Interest on Equity (Juros sobre Capital Próprio - JCP)

The text extinguishes the Interest on Equity (JCP), currently used by companies for paying shareholders and which allows the entrepreneur to invest their money in the company itself.

Taxation on dividends

Currently, dividends are exempt in Brazil. With the reform, the taxation of profits and dividends distributed by companies to individuals or legal entities will be 15%.

According to the basic text approved by the Chamber on September 1st, the charge would be 20%, but during the voting round for the highlights in the following day, there was a reduction to 15%.

Exemptions

Companies opting for Simples Nacional and companies taxed on the presumptive profit with annual sales of up to BRL 4.8 million are exempt from paying the tax.

The exemption also affects:

- supplementary social security funds;

- companies participating in a holding company;

- companies that receive funds from real estate developers subject to the special taxation regime of segregate estate.

Holdings and offshores

The provisions that required the calculation of actual profit for real estate holdings and changed the rules for taxation of profits of offshore companies (companies located in countries with favored taxation) were removed from this version of the text.

Tax support for individuals and companies

Domingues e Pinho Contadores has service centers dedicated to individuals and companies. The teams guide taxpayers throughout the entire fiscal year, ensuring security in actions and compliance with current rules.

This support helps businesses and investors to assess the impacts of changes and adapt tax planning, in order to maintain efficient and strategic management in any scenario.

How may DPC help your company?

Domingues e Pinho Contadores has a specialized team ready to assist your company.

Contact us by email at dpc@dpc.com.br

See more

Sign up for our Newsletter:

Are you interested?

Please contact us, so we can understand your demand and offer the best solution for you and your company.

Rio de Janeiro

Av. Rio Branco 311, 4º e 10º andar - Centro

CEP 20040-903 | Tel: +55 (21) 3231-3700

São Paulo

Rua do Paraíso 45, 4º andar - Paraíso

CEP 04103-000 | Tel: +55 (11) 3330-3330

Macaé

Rua Teixeira de Gouveia 989, sala 302 - Centro

CEP 27910-110 | Tel: +55 (22) 2773-3318